Problems We Solve

Managing wealth is complex. We make it simple with expert advice and smart tech.

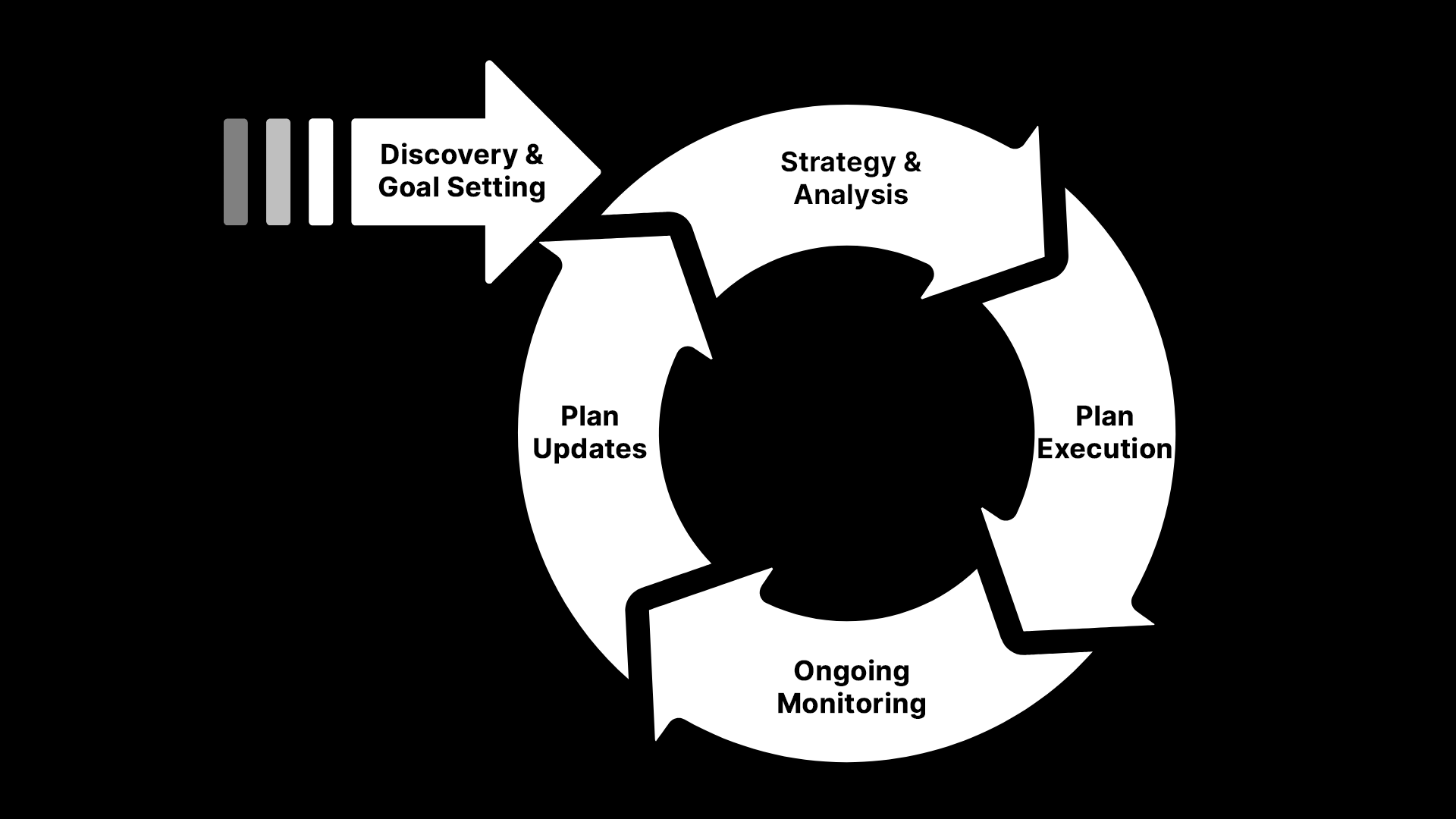

The DePaolo & May Experience

We take a four pillar approach to optimize your finances.

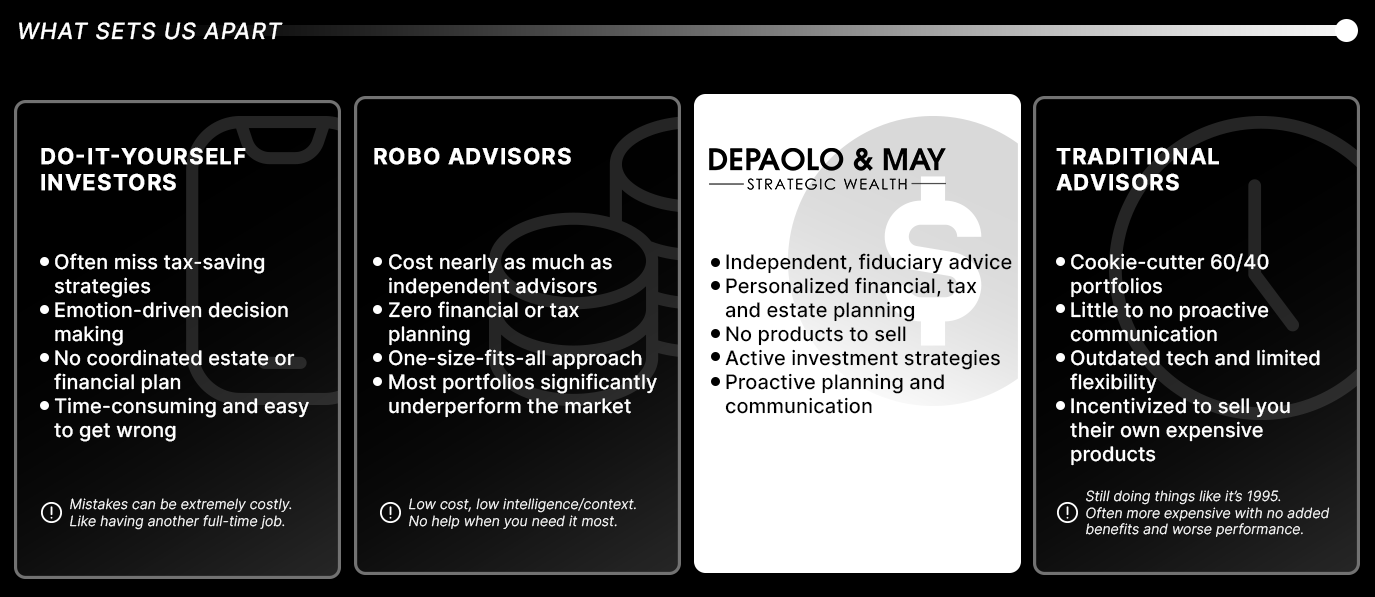

Why We're Different

We're a fee-only, fiduciary, independent financial advisor. We only work in your best interest.

We're a fee-only, fiduciary, independent financial advisor. We only work in your best interest.

100% Transparent - No opaque fees. No vague strategies. Just clear insight into performance, intentions, and market outlook.

100% Transparent - No opaque fees. No vague strategies. Just clear insight into performance, intentions, and market outlook.

Direct Access - No layers. No delays. You'll get real ongoing conversations with the firm's partners.

Direct Access - No layers. No delays. You'll get real ongoing conversations with the firm's partners.

No Cookie-Cutter Approach - We reject static portfolios, overpriced mutual funds, and one-size-fits-all retirement plans.

No Cookie-Cutter Approach - We reject static portfolios, overpriced mutual funds, and one-size-fits-all retirement plans.

Who We Serve

Designed With You in Mind

Sarah and Michael were earning over $800K combined, but their financial life was chaos. They had seven different 401(k)s and investment accounts from previous employers, a pile of RSUs vesting quarterly, a new $2.3M mortgage, two kids under three, and zero tax strategy. They were saving aggressively but had no idea if they were on track — or even what "on track" meant for them.

We consolidated their scattered accounts, built a sleeve-based portfolio aligned with their 15-year timeline to financial independence, and created a proactive tax plan with our CPA partner to manage Sarah's equity comp. We mapped out college funding, modeled early retirement scenarios, and set up estate planning documents they'd been avoiding.

Within six months, Sarah & Michael went from financial stress to clarity. They're saving over $40K annually in taxes through strategic Roth conversions and tax-loss harvesting, and they have a clear roadmap to retire at 50 if they choose. They have confidence in and control over their path forward.

Linda had been a diligent saver for decades — $2.4M across her 401(k), IRAs, and taxable accounts — but her recent divorce left her navigating retirement planning alone for the first time. She had no plan for how to retire. When should she take Social Security? How much could she safely spend? What about healthcare before Medicare? Her accounts were a mix of random funds, and she worried a market downturn in her first years of retirement could derail everything.

We built a comprehensive retirement income plan: optimized Social Security timing (delaying to 67 increased her lifetime benefit by $180K), created a tax-efficient withdrawal strategy across account types, and designed a sleeve portfolio separating growth assets from several years of cash reserves. We modeled healthcare costs and set up a bridge plan until Medicare. We stress-tested her plan against recession scenarios and updated her estate documents post-divorce.

Linda retired at 64 — a year early — with total confidence. She's drawing $135K annually (adjusted for inflation) from her portfolio, her Social Security is maximized, and her healthcare is covered. Her portfolio weathered the recent volatility without panic because her spending needs are secured in the cash sleeve. She's traveling, spending time with grandkids, and living the retirement she worked 40 years to earn — on her own terms.

Jennifer sold her dental practice for $4.8M — a life-changing event that came with overwhelming complexity. She faced a significant tax bill, had no idea how to invest the proceeds, and was paralyzed by the fear of making a costly mistake. Tom was still working but wanted to retire within two years. They needed a plan to make this wealth last for 40+ years.

We immediately coordinated with their CPA and attorney to structure the sale for maximum tax efficiency through installment sales and asset categorization. We built a custom portfolio using our theme-based framework, balancing growth with capital preservation. We modeled multiple retirement scenarios, stress-tested spending levels, and created a phased retirement plan for Tom.

Jennifer & Tom minimized their tax burden through proactive structuring and spread tax liability over multiple years. Their portfolio is positioned for long-term growth with controlled risk. They retired together 18 months post-sale, traveling extensively while their wealth continues to compound. They went from anxiety to confidence — knowing they'll never have to work again.

David built a thriving HVAC business generating $1.2M in annual profit, but nearly all his wealth was locked in the company. He was paying too much in taxes, had no diversified investments, and didn't know whether to reinvest profits, take distributions, or start planning an exit. His estate plan was outdated, and he had no succession strategy.

We worked with David and his CPA to restructure distributions for tax efficiency, established a Solo 401(k) to shelter up to $72K annually, and began systematically moving cash out of the business into a diversified portfolio. We introduced him to M&A advisors to begin informal succession planning and updated his estate documents to protect the business and his family.

David now has $1.8M in invested assets outside the business — real wealth he can access and control. His tax bill dropped by $85K in year one through strategic entity planning and retirement contributions. He's on track to sell the business in 5-7 years with a clear transition plan, and he finally feels like he's building wealth beyond the company.

Note: These scenarios represent the types of real situations we regularly encounter and help families navigate.

Names, details, and specific circumstances have been changed or generalized to protect privacy and do not represent any individual clients.

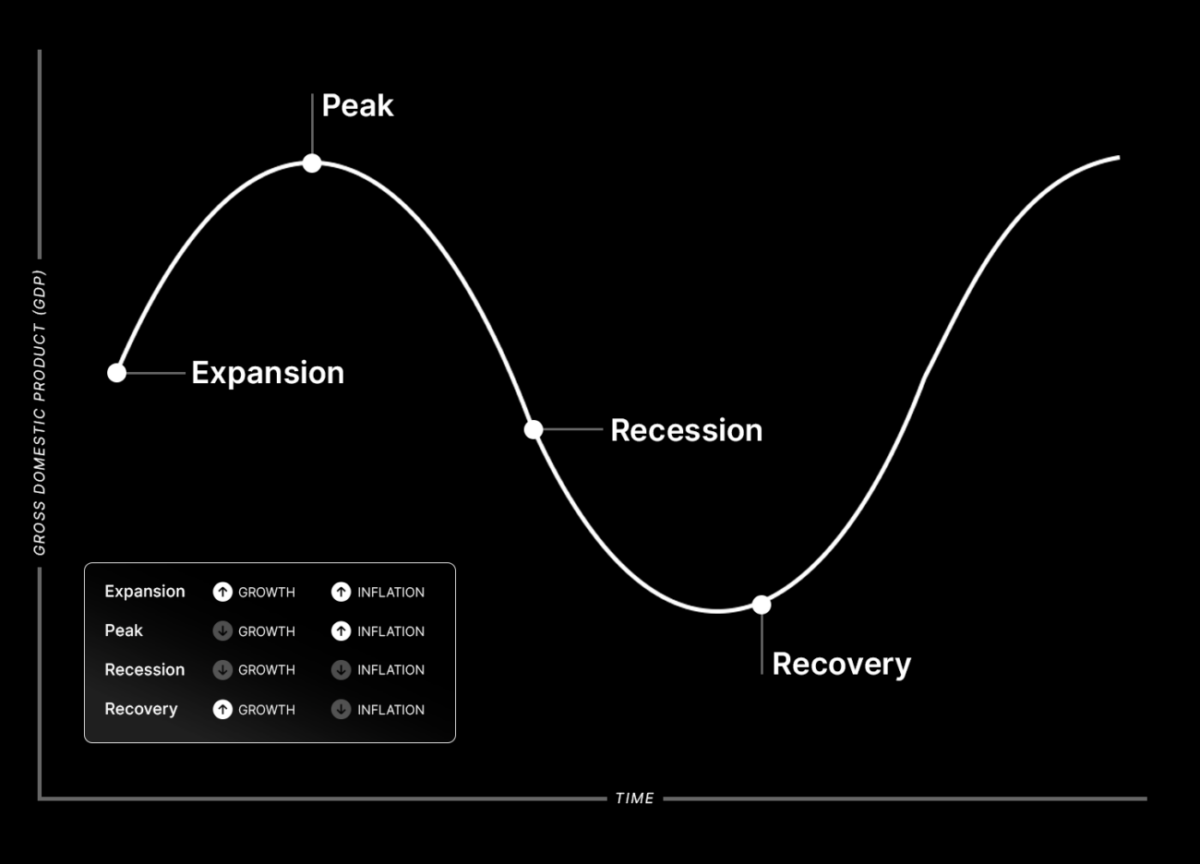

How We Invest

We take a data-driven, tactical approach to active management. Our investment strategy is anchored in the prevailing growth and inflation environment, recognizing that different phases of the business cycle favor different asset classes, sectors, and factors. By rotating exposure accordingly and refining allocations with fundamental and technical insights, we aim to build optimized portfolios for each macroeconomic backdrop.

How We Plan

We believe financial planning starts with what matters most to you. At it's core, your plan should be built around your goals, values, and how you want to use your wealth—both now and in the future. It is about understanding what you care about, what you want to accomplish, and helping you build a thoughtful strategy to get there.

Your Options for Managing Wealth

Our Partners & Technology

Our Partners & Technology

Strategize With Us

Ready to achieve your financial goals?

Or fill out the form and we'll reach out within 24 hours.