2024 Year in Review & 2025 Outlook

IN REVIEW: 2024

Perhaps the overriding theme for 2024 was that of US Resilience. Strong GDP and earnings growth in the US stood in stark contrast to much of the rest of the world. Seven Fed cuts to interest rates that were forecasted to start the year gave way to merely four, as a steady stream of positive surprises throughout the year bolstered the US outlook.

ECONOMICS

The US experienced a “Goldilocks” scenario for most of 2024: good growth with declining inflation. After stuttering briefly to start the year, GDP growth held strong through the remainder. GDP looks set to ultimately come in just under 3% year-over-year growth for 2024, significantly higher than original projections of 1.3%.

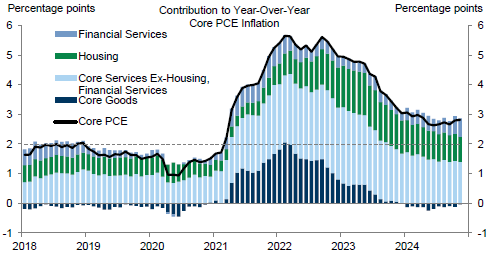

Inflation, meanwhile, continued to move down towards its target (albeit more slowly). Inflation is now hovering around 3% year-over-year, but looks even better on a 6-month annualized basis. By that measure, CPI is currently just 1%. Services (including housing) inflation has remained elevated, offset by good prices which experienced deflation for much of the year. This sticky inflation and economic strength has recently given the Fed pause as it continues to adjust interest rate policy. This Last Mile of Inflation – getting down from 3 to 2% – will likely be front and center as a challenge for 2025.

Inflation (Core PCE) and its Component Parts

Source: Goldman Sachs

FINANCIAL MARKETS

Equity markets soared again in 2024, with the S&P 500 up nearly 25%. Upside surprises to economic growth and company earnings, along with the Fed cutting interest rates, paved the way for strong equity performance. The “Magnificent 7” lead the way, and rightfully so – they averaged more than 30% earnings growth for the year vs all other S&P 500 companies 4% average.

US Resilience again was the theme – virtually no other global equity market performance came close. Among the closest were Canada and China, returning around 15%. The Eurozone only returned around 2% in aggregate. Many of these areas have experienced near-zero GDP growth in recent quarters.

Despite the Fed’s interest rate cuts, bonds struggled for much of the year, as upside growth surprises and sticky inflation kept yields volatile. Given this backdrop, however, gold and commodities did well.

ELECTION RESULTS

With Donald Trump set to begin a second term as president, several areas of the market made significant moves to close the year. Deregulation, a generally more tech and crypto-friendly administration, and a shakeup in the healthcare and food spaces were among the dominant post-election themes. These themes and others will present opportunities into 2025 and beyond.

CURRENT CONDITIONS

While US Resilience remains a dominant theme, three of our firm’s six indicators are currently signaling caution. Inflation is somewhat sticky, which impacts interest rates and the associated availability of credit. And with the recent push from the new administration to cut deficit spending, a concern is rising that this may meaningfully impact government spending and its growth impulse. Government spending in recent years has been a non-trivial component of GDP. Meanwhile, the labor market has softened but moderated with unemployment stabilizing at a healthy 4.2%, reflecting a more balanced employment landscape. The Fed’s gradual rate cuts underscore its confidence in managing inflation expectations, but persistent price pressures in areas like housing and services signal that vigilance remains necessary.

WHAT’S AHEAD

The 2025 outlook reflects a complex but resilient U.S. economy navigating persistent inflation pressures, evolving fiscal and monetary policy, a new administration in Washington, and global uncertainties.

Wage and housing pressures on inflation remain elevated, but have been softening. Trump policies on immigration and tariffs may push in the opposite direction, at least in the near term, stoking inflation further. Notably, investors have already pushed Treasury yields back to recent highs, with the 10-Year poised to break 5% for the first time since the early 2000s.

Moreover, while the incoming administration may be able to reign in government spending somewhat, there is clearly concern over the path of US government debt levels. The extent to which these policies, and resulting Fed actions with interest rates, weigh on growth remains to be seen.

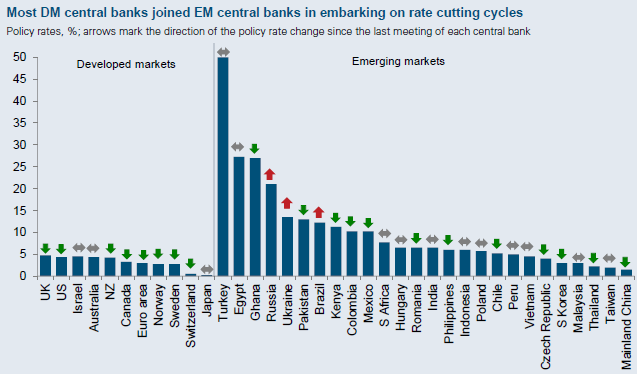

While US Resilience remains the domestic theme, the picture is less robust around the globe. Much of Europe is experiencing no growth, and China is struggling to kick start their sputtering economy. This may begin to weigh on US growth if it continues, but to-date has not been particularly problematic. Globally coordinated policy easing may help reverse this trend.

Central Banks Around the World are Cutting Interest Rates

Source: Goldman Sachs

We anticipate a volatile Q1 in financial markets, driven by the transition to the new administration and uncertainties surrounding Trump’s policies. It’s our belief a large risk to equity prices stems from potential deficit reduction measures. While there are discussions around tax cuts and deregulation, those alone may not offset such a fiscal drag. Markets will likely react sharply to any serious proposals to address the deficit, using sell-offs to signal disapproval and deter the administration from moving forward. Given the heightened focus on Trump’s agenda, with every proposal scrutinized and debated in real time, the coming months will see elevated market sensitivity to policy headlines, underscoring the need for cautious positioning.

2025 SCENARIOS

BEST CASE

In our Best Case scenario, inflation continues its decline, nearing the Fed’s 2% target by year-end. This enables the Fed to reduce rates further, fostering an environment of accommodative monetary policy without overly restrictive real yields. Several stimulative rate cuts, paired with a resilient consumer and robust private sector balance sheets, drive GDP growth to a healthy 2%+. Inflation expectations remain well anchored, providing stability across markets. Treasury yields recede from recent highs.

Equities lead the way, outperforming bonds as investors embrace risk amid strong macroeconomic conditions. Valuations remain elevated but justified by earnings growth, particularly in sectors benefiting from innovation and deregulation. Thematic equities propel market gains in areas exposed to AI, deregulation, healthcare innovation and others.

Bonds also perform well as yields decline alongside the Fed’s successful inflation management. Global markets add a tailwind as geopolitical tensions ease and synchronized policy actions support economic expansion, reversing what has otherwise been sluggish global growth. Alternatives post good returns as well.

New tariff and immigration policy is minimally disruptive. Tariffs evolve more as negotiating tools, while immigration simply mirrors prior-year Trump and Obama-era numbers in net migration flows. Wage pressures and growth are largely unaffected.

BASE CASE

In our Base Case scenario, inflation moderates but remains stubbornly above the Fed’s 2% target, hovering around 2.5% by year-end. This keeps the Fed cautious, leading to measured rate cuts throughout the year to avoid stifling economic momentum. GDP growth slows to around 1.5%, reflecting a “growing but slowing” economy as consumer spending softens and fiscal tightening begins to weigh on overall activity.

Equities deliver modest gains, supported by stable corporate earnings and a focus on innovation-driven sectors. This enables valuations to remain somewhat elevated. Investor sentiment remains balanced as markets adjust to slower growth and an environment of heightened policy uncertainty, particularly around fiscal and regulatory changes.

Bonds offer competitive returns, as gradually declining yields support fixed-income markets. Short-duration bonds remain attractive for their yield stability, while longer-dated securities may benefit, albeit through volatility, from incremental rate cuts.

Overall, markets remain stable but less exuberant than in a Best Case scenario. Investors benefit from a diversified approach, balancing opportunities in quality equities with reliable returns in short duration fixed income, as 2025 unfolds with measured optimism amid a complex economic landscape.

WORST CASE

In our Worst Case scenario, inflation proves more persistent than anticipated, stabilizing around 3% or higher, well above the Fed’s 2% target. This forces the Fed to halt rate cuts and potentially reconsider tightening monetary policy. Elevated inflation erodes consumer purchasing power, while higher borrowing costs weigh on corporate investment and economic activity. GDP growth is buoyed for some time, but begins to crack in the face of higher inflation and diminished confidence, both from consumers and businesses.

Equities struggle under these conditions, as valuations come under pressure from elevated interest rates and rising input costs. Risk-off sentiment dominates, with investors rotating out of equities and into safer assets. Sectors reliant on discretionary spending or sensitive to higher financing costs, such as technology and real estate, face significant headwinds.

Bonds offer mixed results. While safe-haven demand may support government securities, rising yields in response to inflationary pressures weigh on longer-duration fixed income. Credit spreads widen as economic uncertainty raises concerns about corporate solvency, particularly in more leveraged sectors.

In this environment, diversification and a defensive posture are critical. Short-duration bonds, alternatives, and cash-like instruments outperform riskier assets, helping investors weather the challenges of a high-inflation, low-growth scenario. Patience and prudent risk management are essential as markets navigate a turbulent 2025.

In the alternative, there exists a small but non-zero probability that the weight of higher interest rates finally begins to crack consumers and businesses. In particular, businesses face refinancing on debts they are unable to afford. Confidence comes severely under pressure. Under these conditions, inflation and GDP would likely come in materially lower. Equities would likely experience a more severe drawdown, offset by higher bond performance in a risk-off trade and alongside a Fed likely to significantly cut interest rates.

2025 EQUITY THEMES

CLOSING THOUGHTS

As we look ahead to 2025, the U.S. remains a focal point of strength, fueled by resilient consumers and a steady, if cautious, Federal Reserve. Yet we see no shortage of complexity—from persistent inflation pressures, to evolving policy under the new administration, to softer global growth. In this environment, we expect periodic market volatility, especially in response to shifting policy signals and ongoing debates around deficit reduction and other government policy.

That said, opportunities remain robust. Innovation in areas like AI and healthcare continues to drive value, and sectors poised to benefit from deregulation, demographic shifts, and other themes all offer compelling potential. Disciplined risk management will remain essential, given the range of possible scenarios—from a continued “Goldilocks” scenario where inflation recedes and growth remains, to a more challenging outcome if inflation proves stubborn and/or growth weakens.